Mastering Time Series Analysis for Market Forecasting in Econometrics

Deciphering Time Series Analysis in Econometrics: A Gateway to Forecasting Future Market Trends

In the constantly evolving world of technology and business, understanding and predicting market trends is essential for driving successful strategies. This is where the mathematical discipline of econometrics becomes crucial, particularly in the domain of Time Series Analysis. Given my background in artificial intelligence, cloud solutions, and machine learning, leveraging econometric models has been instrumental in foreseeing market fluctuations and making informed decisions at DBGM Consulting, Inc.

What is Time Series Analysis?

Time Series Analysis involves statistical techniques to analyze time series data in order to extract meaningful statistics and other characteristics. It’s used across various sectors for forecasting future trends based on past data. This method is particularly significant in econometrics, a branch of economics that uses mathematical and statistical methods to test hypotheses and forecast future patterns.

The Mathematical Backbone

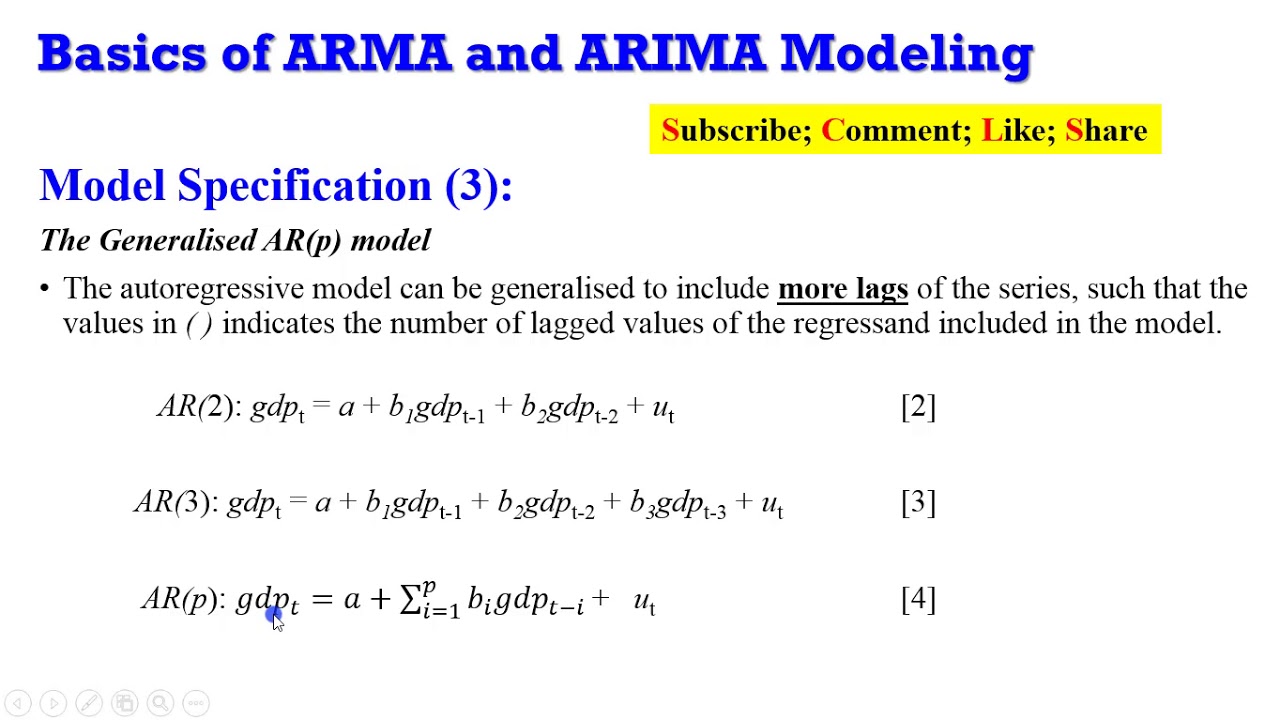

The mathematical foundation of Time Series Analysis is built upon models that capture the dynamics of time series data. One of the most commonly used models is the Autoregressive Integrated Moving Average (ARIMA) model. The ARIMA model is denoted as ARIMA(p, d, q), where:

- p: the number of autoregressive terms,

- d: the degree of differencing,

- q: the number of moving average terms.

This model is a cornerstone for understanding how past values and errors influence future values, providing a rich framework for forecasting.

Embedding Mathematical Formulas

Consider the ARIMA model equation for a time series \(Y_t\):

\[Y_t^\prime = c + \Phi_1 Y_{t-1}^\prime + \cdots + \Phi_p Y_{t-p}^\prime + \Theta_1 \epsilon_{t-1} + \cdots + \Theta_q \epsilon_{t-q} + \epsilon_t\]

where:

- \(Y_t^\prime\) is the differenced series (to make the series stationary),

- \(c\) is a constant,

- \(\Phi_1, \ldots, \Phi_p\) are the parameters of the autoregressive terms,

- \(\Theta_1, \ldots, \Theta_q\) are the parameters of the moving average terms, and

- \(\epsilon_t\) is white noise error terms.

Applying ARIMA in forecasting involves identifying the optimal parameters (p, d, q) that best fit the historical data, which can be a sophisticated process requiring specialized software and expertise.

Impact in Business and Technology

For consulting firms like DBGM Consulting, Inc., understanding the intricacies of Time Series Analysis and ARIMA models is invaluable. It allows us to:

- Forecast demand for products and services,

- Predict market trends and adjust strategies accordingly,

- Develop AI and machine learning models that are predictive in nature, and

- Assist clients in risk management by providing data-backed insights.

This mathematical foundation empowers businesses to stay ahead in a competitive landscape, making informed decisions that are crucial for growth and sustainability.

Conclusion

The world of econometrics, particularly Time Series Analysis, offers powerful tools for forecasting and strategic planning. By combining this mathematical prowess with expertise in artificial intelligence and technology, we can unlock new potentials and drive innovation. Whether it’s in optimizing cloud solutions or developing future-ready AI applications, the impact of econometrics is profound and pivotal.

As we continue to advance in technology, methodologies like Time Series Analysis become even more critical in decoding complex market dynamics, ensuring businesses can navigate future challenges with confidence.

For more insights into the blending of technology and other disciplines, such as astrophysics and infectious diseases, visit my blog at https://www.davidmaiolo.com.